The Coinbase Card is the most widely available crypto debit card for US residents — but is it the best option, or just the most convenient? With its seamless integration into the largest US-regulated crypto exchange, no annual fee, and rotating 4% cashback categories, the Coinbase Visa looks attractive on the surface . But hidden costs — including a 2.49% foreign transaction fee, withdrawal fees at the free tier, and spreads baked into every crypto conversion — can eat away at your rewards. This comprehensive 2026 review analyzes every aspect of the Coinbase Card: its fee structure, cashback mechanics, tax implications, and how to optimize your spending to earn maximum crypto rewards. We’ll also compare it directly to US competitors like Gemini Credit, MetaMask, and Bleap, and answer the ultimate question: Is the Coinbase Card worth its fees, or are better options available?

The Coinbase Card has no annual fee and offers up to 4% crypto cashback — but those headline numbers obscure real costs. The 2.49% foreign transaction fee on non-USD purchases is among the highest in the crypto card market. The spread between Coinbase’s conversion rate and the mid-market rate can add another 0.5-1% to every crypto-funded purchase. And ATM withdrawals come with both Coinbase fees and operator fees unless you pay $4.99/month for Coinbase One . If you spend primarily in USD, earn the maximum 4% cashback, and avoid crypto conversion by spending from a USD balance, the card can generate positive value. But for international travelers or anyone spending crypto directly, the fees quickly erode — or even exceed — the cashback earned .

📖 Coinbase Card Overview: What It Is and Who It’s For

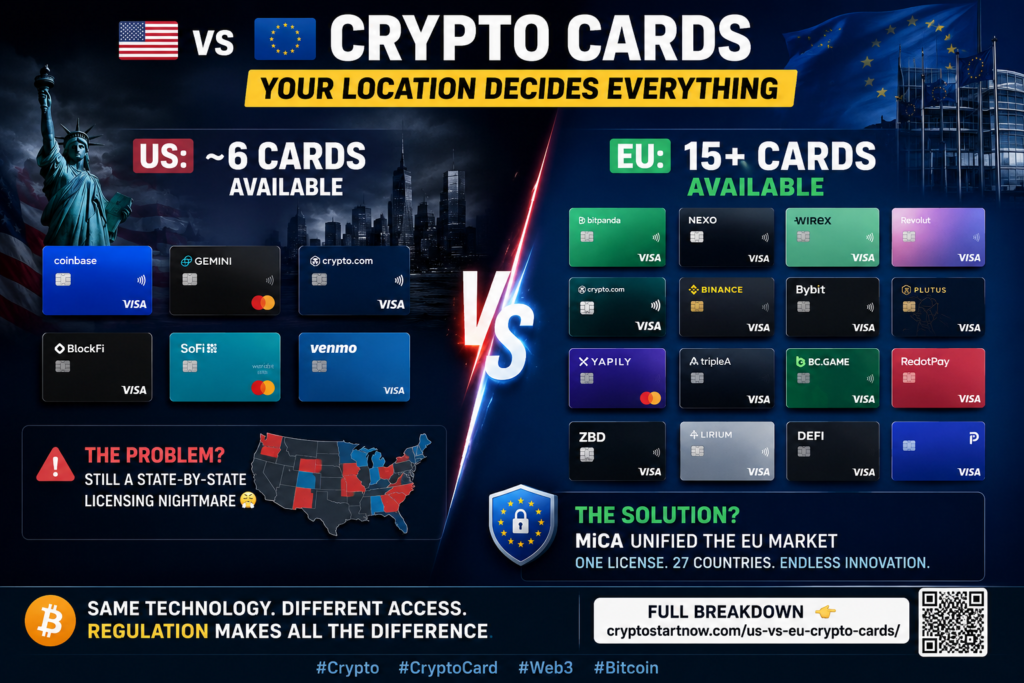

The Coinbase Card is a Visa debit card that links directly to your Coinbase exchange account. Launched in 2019 and expanded significantly since, it’s currently available to eligible users in the United States, the United Kingdom, and select European countries (though EU availability has been reduced in some markets) .

Unlike self-custody cards that require managing private keys and gas fees, the Coinbase Card offers a familiar banking experience: you spend from your Coinbase balance, the card works anywhere Visa is accepted, and you earn crypto rewards on most purchases. The card is available in both virtual and physical formats, with the physical card supporting ATM withdrawals .

🇺🇸 US Card (Visa)

The US version of the Coinbase Card is a Visa debit card that spends from your USD balance by default. If your USD balance is insufficient, it can spend from your crypto balances (USDC, BTC, ETH, etc.) with a conversion spread .

🇪🇺 EU Card (Visa) — Discontinued/Reduced

Coinbase discontinued its EU-issued Visa card in 2023 due to partnerships with Paysafe ending. European users now have limited options, primarily the Coinbase card issued through other partners with different terms .

| Feature | Coinbase Card (US) | Coinbase Card (EU/UK) |

|---|---|---|

| Network | Visa | Visa |

| Card Type | Debit | Debit |

| Custody Model | Custodial (Coinbase holds funds) | Custodial |

| Annual Fee | $0 | $0 |

| Monthly Fee (Coinbase One) | $4.99 (optional) | £4.99 / €4.99 (optional) |

| Cashback (Standard) | Up to 4% (rotating categories) | Up to 4% (rotating) |

| US Availability | ✅ 50 states | ❌ |

| EU/UK Availability | ❌ | ✅ (reduced, partners) |

💰 Coinbase Card Fees: Complete Breakdown

The fee structure is the most critical factor in determining whether the Coinbase Card saves or costs you money. Here’s the complete breakdown for US users .

| Fee Type | Standard Rate | Coinbase One Rate (US $4.99/mo) | Notes |

|---|---|---|---|

| Annual Fee | $0 | $0 (plus monthly subscription) | No annual fee |

| Monthly Subscription | $0 | $4.99/month | Coinbase One includes fee waivers |

| Crypto Conversion | Spread only (0.5-2% estimated) | Spread only | No separate conversion fee, but spread applies |

| Foreign Transaction Fee | 2.49% | 2.49%

道的Not waived by Coinbase One | |

| ATM Withdrawal (domestic) | $2.50 + operator fee | $0 + operator fee | Coinbase One waives the $2.50 fee only |

| ATM Withdrawal (international) | $2.50 + operator fee + 2.49% FX | $0 + operator fee + 2.49% FX | International ATM uses FX fee too |

| ATM Withdrawal Limit | $1,000/day (standard) | $1,000/day | Higher for Coinbase One? — Verify |

| Card Replacement Fee | $0 for first, $4.95 thereafter | $0 | Coinbase One waives replacement fees |

You have $0 USD and 100 USDC in your Coinbase account. You make a $50 purchase at a US store. Coinbase converts USDC to USD at the current rate, applying a spread of roughly 0.5% (varies). If the market rate is 1 USDC = $1.000, you might receive an effective rate of $0.995 per USDC. You spend approximately 50.25 USDC to cover $50. Total cost: $0.25 on $50 (0.5%) — plus you earn cashback .

You have a $0 USD balance and 100 USDC. You spend €50 in France (approx $54 USD). Coinbase converts USDC to USD (spread ~0.5%), then converts USD to EUR at Visa’s rate plus the 2.49% FX fee. On a $54 purchase: spread cost ~$0.27 + FX fee ~$1.34 = total cost $1.61 (3.0%). If you’re earning 1-4% cashback, international spending may net to negative or breakeven at best. Do not use the Coinbase Card for foreign currency purchases if you have a better 0% FX card option .

🏆 Coinbase Card Cashback: How to Maximize Crypto Rewards

The Coinbase Card’s primary value proposition is cashback paid in crypto. Unlike many card issuers that require staking or specific asset holdings, Coinbase offers straightforward rotating reward categories .

| Reward Category | Cashback Rate | Reward Asset Options | Notes |

|---|---|---|---|

| Rotating 4% Category | 4% (temporary, changes quarterly) | Stellar (XLM) typically — sometimes other assets | Limited to specific merchant categories |

| Standard Crypto Rewards | 1% | Bitcoin (BTC) or other selected assets | Default reward on all eligible purchases |

| USDC Rewards (with Coinbase One) | 4% on USDC balance (separate from card) | USDC | Not card spending — separate holding yield |

| Promotional Bonuses | Temporary | Various | Check current Coinbase promotions |

- 1. Choose the 4% rotating category each quarter: Coinbase regularly updates a high-yield category (e.g., groceries, dining, gas, travel). Set a reminder to activate it, then concentrate your spending in that category during the promotional period .

- 2. Opt for XLM (Stellar) rewards when available: The 4% rotating category often pays in Stellar (XLM). While XLM is volatile, the 4% rate is significantly higher than the 1% base. Convert XLM to USDC or BTC immediately to lock in value (watch for tax implications).

- 3. Spend from your USD balance — not crypto: To avoid conversion spreads entirely, deposit USD to your Coinbase account via ACH transfer (free) or wire. Spend directly from your USD balance. You still earn cashback, but you bypass crypto conversion fees .

- 4. Use the card only for USD-denominated purchases: The 2.49% FX fee makes international spending unattractive. For travel, pair the Coinbase Card with a 0% FX crypto card like MetaMask Metal or Gemini Credit (both available in the US).

- 5. Consider Coinbase One for heavy ATM users: If you frequently withdraw cash from ATMs, the $4.99/month Coinbase One subscription eliminates the $2.50 per ATM withdrawal fee (though operator fees still apply). For 3+ ATM withdrawals per month, it pays for itself .

💳 Coinbase One: Is the $4.99 Monthly Subscription Worth It?

Coinbase One is a premium subscription that bundles several benefits for a flat monthly fee. Here’s what you get and whether it makes financial sense .

| Benefit | Without Coinbase One | With Coinbase One ($4.99/mo) | Value Estimate |

|---|---|---|---|

| ATM Withdrawal Fee (domestic) | $2.50 per withdrawal | $0 | $2.50 saved per withdrawal |

| Card Replacement | $4.95 after first | $0 | Small savings |

| Trading Fees (Advanced Trade) | Tiered (0-0.6%) | $0 | Potentially high value for traders |

| Gas Fee Rebates | None | Gas fee rebates (ETH network) | Small value for DeFi users |

| Prize Drawings | None | Monthly prize entries | Low expected value |

| 24/7 Phone Support | Email/chat | Priority phone support | Convenience value |

For ATM users: If you make 2 ATM withdrawals per month, Coinbase One saves you $5.00 in fees ($2.50 x 2) — exactly the $4.99 monthly cost. At 3+ withdrawals per month, you come out ahead. For traders: If you trade more than ~$1,000/month in Advanced Trade mode, the $0 trading fee likely justifies the subscription. For casual users: Who rarely use ATMs and trade minimally, Coinbase One is likely not worth the monthly fee .

📊 Coinbase Card vs. US Competitors: Complete Comparison

The US crypto card market is smaller than the EU, but there are several legitimate alternatives to the Coinbase Card .

| Card | Cashback | FX Fee | ATM Fee | Custody | Annual Fee | Best For |

|---|---|---|---|---|---|---|

| Coinbase Card | 1-4% (rotating) | 2.49% | $2.50 (+operator) | Custodial | $0 ($4.99/mo optional) | USD spenders, Coinbase ecosystem users |

| Gemini Credit Card | 1-3% (dining 3%, grocery 2%) | 0% | $0 up to $1k/mo, then $2.50 | Credit (traditional) | $0 | International travelers, credit building |

| MetaMask Metal Card | 3% (first $10k/year) | 0% | 2% after $1,200/mo | Self-custody | $199 | Self-custody advocates, privacy |

| Bleap (MPC) | 2% USDC | 0% | Free up to $400/mo | Non-custodial MPC | $0 | Zero-fee spending with rewards |

| Crypto.com (US) | 1-5% CRO (requires stake) | Varies | Free up to $200-400/mo (tier) | Custodial | $0 (requires CRO lockup) | CRO ecosystem believers |

✅ When the Coinbase Card Wins

- You’re already a heavy Coinbase user — the card integrates seamlessly with your existing account

- You spend primarily in USD (domestic US purchases)

- You actively manage the 4% rotating category and maximize spending there

- You have Coinbase One and make frequent ATM withdrawals

- You prefer simplicity over managing multiple accounts — one app for exchange + card

- You want to earn crypto cashback without staking or holding a specific token

⚠️ When to Choose an Alternative

- You frequently travel internationally — the 2.49% FX fee is a dealbreaker → Gemini Credit (0% FX) or MetaMask Metal (0% FX) are better.

- You want self-custody and true ownership of funds → MetaMask or Bleap.

- You want to build credit history while earning crypto rewards → Gemini Credit Card (only credit card in this space).

- You want the highest possible cashback on all spending without category hunting → Bleap (2% flat) or Gemini (1-3% category-based).

- You need non-USD spending without fees → Avoid Coinbase Card entirely.

The Gemini Credit Card is the strongest alternative for US users who spend internationally — its 0% FX fee alone makes it superior to Coinbase for travel. For self-custody users, MetaMask Metal offers 3% cashback and 0% FX with a $199 annual fee (worthwhile if you spend >$6,600/year abroad). For pure fee minimization, Bleap offers 0% fees + 2% cashback. The Coinbase Card remains competitive primarily for US domestic spenders who are already invested in the Coinbase ecosystem and actively manage their reward categories .

📈 How to Maximize Coinbase Card Rewards — Advanced Strategies

📅 Strategy 1: Rotating Category Optimization

Coinbase’s 4% categories change quarterly (e.g., “groceries” Q1, “gas” Q2, “dining” Q3). At the start of each quarter, activate the category in the Coinbase app. Then shift your spending: buy grocery gift cards at the grocery store during that category to extend the 4% rate to other merchants. This technique can effectively earn 4% on many purchases beyond the limited category.

💱 Strategy 2: Immediate Reward Conversion

If the 4% reward is paid in XLM (or another volatile altcoin), convert your rewards to USDC or BTC immediately after each reward distribution. Set a recurring calendar reminder weekly. This locks in the value of your 4% reward before the token price potentially declines. Note: each conversion is a taxable event in the US.

🏦 Strategy 3: USD First — Crypto Only as Backup

Deposit USD via ACH transfer (free, 3-5 day settlement) into your Coinbase USD balance. Spend directly from this balance. You’ll earn cashback on every purchase without paying any crypto conversion spread. The only cost is the (minimal) spread when you originally bought crypto — not at point of sale.

🔄 Strategy 4: Pair with a 0% FX Card

Use the Coinbase Card exclusively for USD domestic spending (where its 2.49% FX fee doesn’t apply). For international travel, use Gemini Credit Card (0% FX) or MetaMask Metal (0% FX). This “two-card strategy” gives you the best of both worlds: high cashback domestically and no fees abroad.

📊 Strategy 5: Tax-Efficient Reward Management

In the US, crypto rewards from spending are treated as rebates (non-taxable at receipt) but any subsequent appreciation is taxable when sold. To minimize tax complexity, either convert rewards to USDC immediately (reporting minimal gain/loss) or hold long-term for appreciation but track cost basis carefully. Consider using a crypto tax software to automate tracking .

🎯 Strategy 6: Avoid Using Card for Large Crypto Purchases

Coinbase’s spread on buying crypto through the card can be 2-3% higher than using Advanced Trade. Never use the Coinbase Card to “buy crypto” — that defeats the purpose. Use the card for everyday spending, and buy crypto separately on the exchange using limit orders with lower fees .

📋 Real-World Earnings Scenarios — Is the Card Worth It?

Let’s calculate actual net value across different spending profiles, assuming 4% cashback on rotating categories and USD spending .

| Spending Profile | Monthly Spend | Gross Cashback (4% on rotating, 1% on others) | Fees Paid | Net Monthly Value | Net Annual Value |

|---|---|---|---|---|---|

| Heavy optimizer (50% in 4% category) | $2,000 | (0.5*2000*0.04 = $40) + (0.5*2000*0.01 = $10) = $50 | $0 (USD spending, no ATM) | $50 | $600 |

| Moderate user (25% in 4% category) | $1,500 | (0.25*1500*0.04 = $15) + (0.75*1500*0.01 = $11.25) = $26.25 | $0 | $26.25 | $315 |

| International user (50% foreign) | $2,000 ($1k domestic, $1k intl) | $25 (domestic) + $10 (intl 1% base) = $35 gross | $1,000 intl × 2.49% = $24.90 in FX fees | $35 – $24.90 = $10.10 | $121 |

| Heavy ATM user (4 withdrawals/mo, no Coinbase One) | $2,000 spend + $800 cash | $35 cashback ($2k spend) | 4 ATM × $2.50 = $10 in ATM fees | $25 | $300 |

| Heavy ATM user + Coinbase One ($4.99/mo) | $2,000 spend + $800 cash | $35 cashback | $4.99 subscription (ATM fees waived) | $30.01 | $360 |

The Coinbase Card generates positive net value for most domestic spenders who actively manage rotating categories. At $600/year for heavy optimizers, the card is genuinely rewarding. However, international spending severely erodes value — the $24.90 FX fee on $1k monthly international spend reduces net annual value to just $121, which is lower than a free 0% FX card with 1% cashback ($120/year with zero fees). For heavy ATM users, Coinbase One becomes a valuable add-on at 3+ monthly withdrawals .

🔮 Pros and Cons — The Final Verdict

✅ COINBASE CARD PROS

- ✅ No annual fee — zero cost to hold

- ✅ Up to 4% crypto cashback on rotating categories — among highest in US market

- ✅ Seamless Coinbase integration — one app for exchange + card

- ✅ No staking requirements — rewards don’t require locking tokens

- ✅ Works anywhere Visa is accepted — 100M+ merchants globally

- ✅ Virtual card available instantly — can add to Apple/Google Pay

- ✅ Choice of reward assets — XLM, BTC, ETH, etc.

- ✅ Coinbase One adds value for heavy users — ATM fee waiver, zero trading fees

- ✅ Fully regulated US exchange — less regulatory uncertainty than offshore competitors

❌ COINBASE CARD CONS

- ❌ 2.49% foreign transaction fee — among the highest in crypto cards, eliminates value for international spending

- ❌ $2.50 domestic ATM fee (unless you pay $4.99/mo for Coinbase One)

- ❌ Custodial model — funds held on Coinbase exchange, not self-custody

- ❌ Spread on crypto conversion — hidden cost when spending from crypto balance (0.5-2%)

- ❌ Rotating 4% category requires active management — must opt-in each quarter

- ❌ Rewards are taxable — appreciation on rewards is capital gains in US

- ❌ No credit building — debit card doesn’t affect credit score (unlike Gemini Credit)

- ❌ EU availability is limited/closed — primarily a US-focused product

- ❌ Customer support can be slow — common complaint among users

YES — for US residents who spend primarily in USD and actively manage rotating reward categories. The Coinbase Card generates positive net value for domestic spenders, with heavy optimizers earning $500-600 per year in crypto rewards at zero cost. The seamless integration with the Coinbase ecosystem, no staking requirements, and up to 4% cashback make it one of the best crypto debit cards for US users who are already Coinbase customers .

NO — for international travelers, ATM-heavy users (without Coinbase One), or anyone who wants self-custody or 0% FX fees. The 2.49% foreign transaction fee is a dealbreaker for anyone spending significant amounts abroad. For international users, the Gemini Credit Card (0% FX, 1-3% cashback) is unequivocally better. For self-custody advocates, MetaMask Metal or Bleap offer better control and similar or better fees.

The optimal strategy: Use the Coinbase Card for domestic USD spending where you maximize the 4% rotating category. Pair it with a Gemini Credit Card (0% FX) for all international purchases and ATM withdrawals (up to $1k/month free). This two-card combo gives you 1-4% cashback domestically, 0% FX internationally, and no annual fees on either card — the best of both worlds for US crypto spenders .

For Coinbase One: Subscribe if you make 3+ ATM withdrawals monthly OR trade more than ~$1,000/month on Advanced Trade. Otherwise, skip it — the $4.99/month isn’t justified for casual users.

Cryptocurrency analyst with 7+ years of market experience. I write detailed, practical guides to help you navigate crypto with confidence. Follow me on LinkedIn — let’s grow together. 👇

🔗 LinkedIn Profil

🌐 CryptoStartNow — Follow Us Everywhere!

Subscribe to stay updated with new guides and reviews!

📘 Facebook → Facebook